Arne JohannssenStochastische Schadenreservierung unter Verwendung von Zustandsraummodellen und des Kalman-Filters

Finanzmanagement, volume 117

Hamburg 2016, 264 pages

ISBN 978-3-8300-9043-4 (print)

ISBN 978-3-339-09043-0 (eBook)

Rezension

[…] Die vorliegende Arbeit stellt damit die erste Abhandlung dar, die einen eingehenden Überblick über den aktuellen Forschungsstand in Bezug auf den Einsatz von Zustandsraummodellen und des Kalman-Filters in der stochastischen Schadenreservierung liefert.

About this book deutschenglish

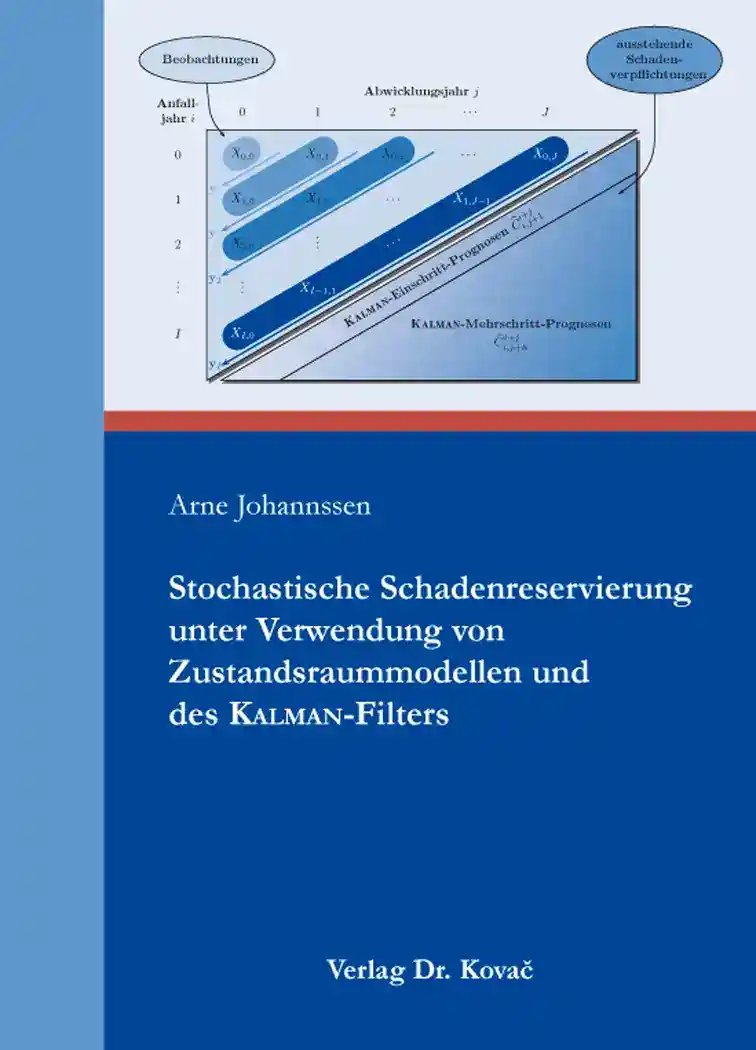

A non-life insurance company faces the situation that the earned premiums are known at the end of the fiscal year but the outstanding loss liabilities are unknown. Therefore, one of the main tasks of actuaries in non-life insurance is to predict the outstanding loss liabilities. The resulting claims reserves are often a big part of the liability side of the balance sheet, so an adequate claims reserving is very important to every non-life insurer.

In this dissertation stochastic claims reserving methods are presented which are based on state space modeling and the Kalman filter algorithms. Therefore, papers in this context are collated and categorized and a new state space model for cumulative payments is presented. Moreover, an empirical comparison of these models and additional popular claims reserving models is performed. This work thus provides a detailed overview of the current state of research in relation to the use of state space models and the Kalman filter in stochastic claims reserving.